- FR

- NL

- EN

The global economy proved more resilient than expected in the first half of 2023, but the growth outlook remains weak

Temps de lecture: 2 min | 02 Oct 2023 à 17:04

With monetary policy becoming increasingly visible and a weaker-than-expected recovery in China, global growth in 2024 is projected to be lower than in 2023. While headline inflation has been declining, core inflation remains persistent, driven by the services sector and still relatively tight labour markets. Risks continue to be tilted to the downside. Inflation could continue to prove more persistent than anticipated, with further disruptions to energy and food markets still possible. A sharper slowdown in China would drag on growth around the world even further. Public debt remains elevated in many countries.

Global growth is expected to remain weak

The world economy is expected to grow by 3.0% in 2023, before slowing down to 2.7% in 2024. A disproportionate share of global growth in 2023-24 is expected to continue to come from Asia, despite the weaker-than-expected recovery in China.

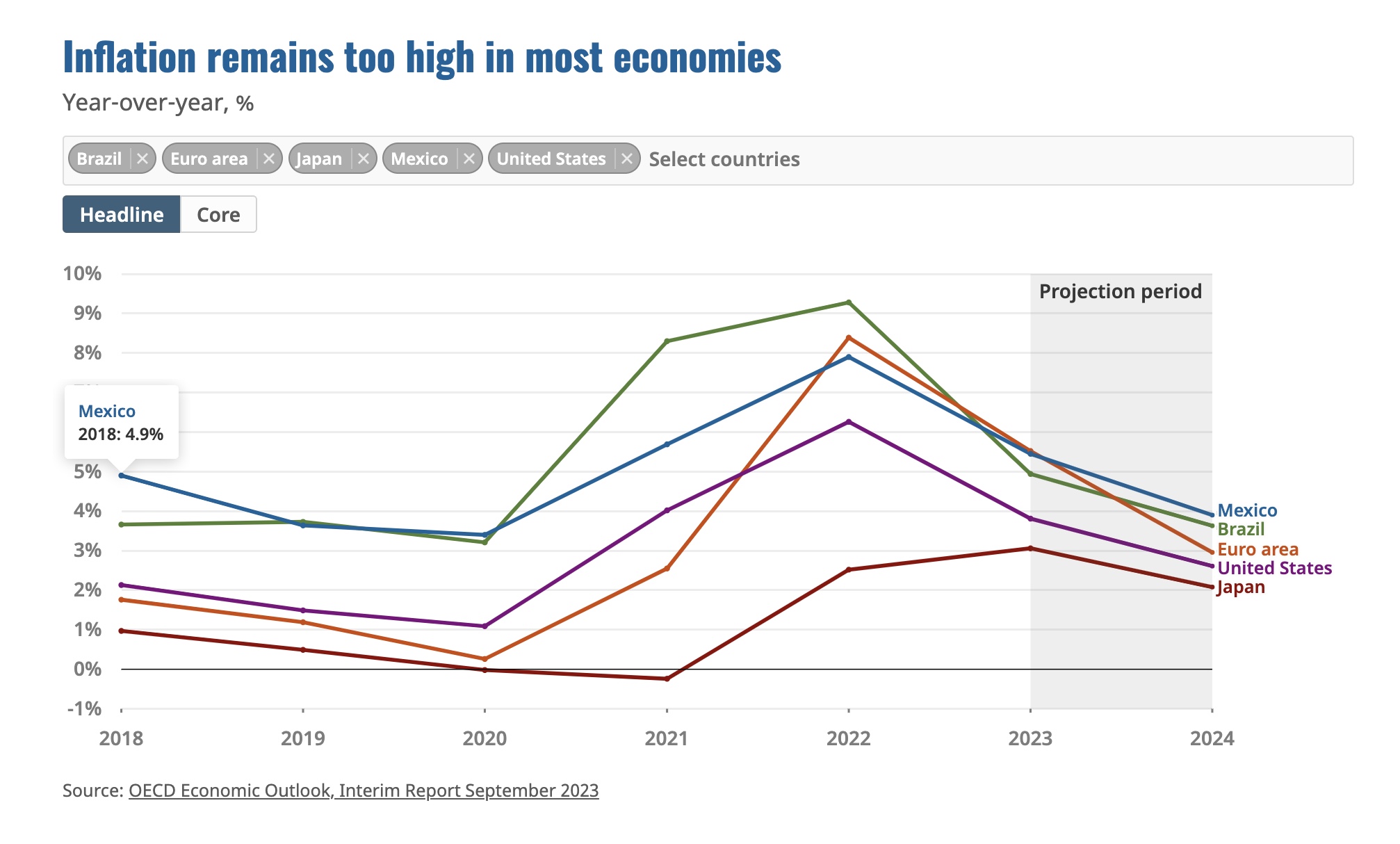

Headline inflation is coming down but core inflation remains persistent

Headline inflation has continued to come down in many countries, driven by the decline of food and energy prices in the first half of 2023. However, core inflation – inflation excluding the most volatile components, energy and food – hasn’t significantly slowed. It remains well above central banks’ targets. A key risk is that inflation could continue to prove more persistent than expected, which would mean interest rates need to tighten further or remain higher for longer.

More information

OCDE (2023), OECD Economic Outlook, Interim Report September 2023 : Confronting Inflation and Low Growth, Éditions OCDE, Paris, https://doi.org/10.1787/1f628002-en.

The near-term global outlook is shaped by the increasingly visible impact of monetary policy tightening by most major central banks and stresses in the Chinese economy. Global growth is projected to slow, remaining below trend in 2023-24, while inflation moderates but remains above target. Key downside risks include the possibility of a sharper-than-expected slowdown in China and a continued rise in oil prices.

The Interim Report says that monetary policy should remain focused on bringing inflation back to target, while increased efforts by governments are needed to rebuild fiscal space and respond to future challenges, including the climate transition. Structural policy efforts need to be reinvigorated to strengthen growth prospects, with a key priority being to revive global trade. The Interim Report is an update on the assessment in the June 2023 issue of the OECD Economic Outlook (Number 113).

Mots clés

Abonnez-vous à notre newsletter

Recevez toutes les actualités publiées par notre communauté